The long and the short of IT

What to do with the gains in H2

The TechMark Index is +14.2% YTD - woohoo. The gain was all made in the past few months (see below). Somewhat confusingly, UK tech TSR is -10.46% YTD, from +11.02% for cal24. Why the difference? Tech investing continues to favour large companies over small, and for this summer prefers the wider constituents of TechMark (i.e. industrials, Defence, Electronics, Gambling etc) rather than software and IT Services. In addition, while smaller companies offer some superb individual company out-performance the category is -11.5% YTD with midcaps being 11-% YTD. In a sector where growth and innovation are cherished, investors want companies with large established customer franchises, rather than the start-ups and up-starts. We explore what else is afoot in this season of pennies from heaven?

Tech Universe results and updates this week span Data & Analytics (Monday.com); IT Infrastructure Services (Cancom); UK Hardware (Xaar); IT Professional Services (Netcompany); Gaming (Trufin); IaaS (Coreweave, Rackspace, Beeks Financial); Recruitment (PageGroup, Randstad); IoT/Smart (Aurrigo); Travel-Tech (Weibo). Read on. Data insights (not navel gazing or ‘vibes’) inform our evolving views on the tech-economy.

Tech drivers and Points to Ponder

1. Small ain’t so beautiful

The TSR data says that UK tech is -10.46% YTD, from +11.02% for cal24. While smaller companies offer some superb individual out-performance but that category is -11.5% YTD, midcaps are 11-% YTD. In a sector where growth and innovate is cherished, investors continue to favour companies with large established customer franchises.

The current YTD top TSR performers are:

Alphawave IP +109.4% (Mkt Cap £1,139m),

Quartix +75% (Mkt Cap £133m), and

Made Tech +62% (Mkt Cap £60m).

The poorest performers are:

Northcoders -80.5% (Mkt Cap £3m),

Iomart -70.5% (Mkt Cap £27m), and

Zoo Digital -64.3% (Mkt Cap £14m).

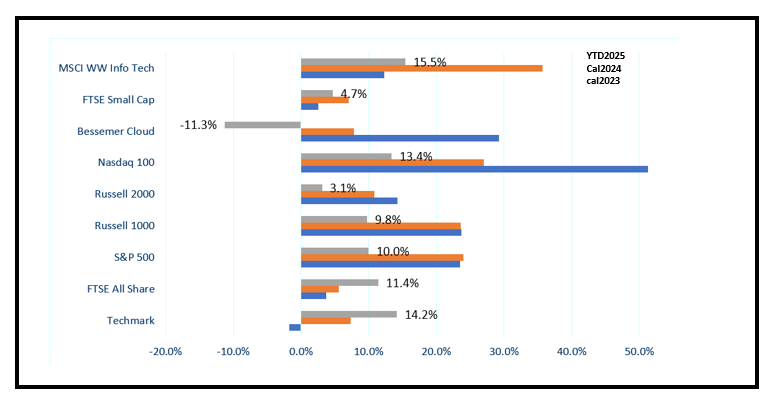

The pattern is repeated in the Index performance with UK small cap +4.7% and Russell 2000 +3.1% (see below). However the market is rallying. The strength of the summer rally (shares +14% since May) has been a surprise the only change of substance has been;

some lightening on Cost of Capital concerns,

a general ‘getting used to the uncertainty’.

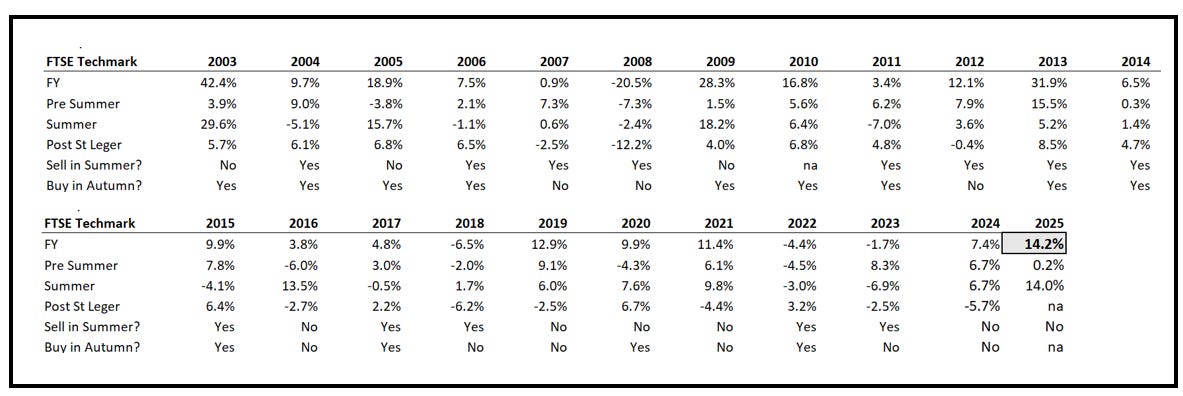

Company guidance remains muted (although Q2 results are in-line/beat). Looking into market seasonality, we see three general phases; pre-summer, summer, and post summer. Usually pundits tell us that it is better to sell in the summer, and then buy the recovery for Q4 (and the hope of the Santa rally).

Looking back to 2003 (i.e. ignoring the memories of the Dotcom crash), of the last 23 years since:

a summer rally occurred in 9 years

Q4 rally happened in 13 years

a summer and autumn rally together in 4 years

a summer rally followed by an autumn downturn in 3 years

the confluence of sell in the summer and buy in the Autumn (i.e. Sell in May and go away . . . ) happened in 8 years

no discernible pattern in many years!

Techmark Index performance: A seasonal view since 2003

Note: Priced 15 August pre-market. Source: Company data, Yahoo Finance, Technology Investment Services

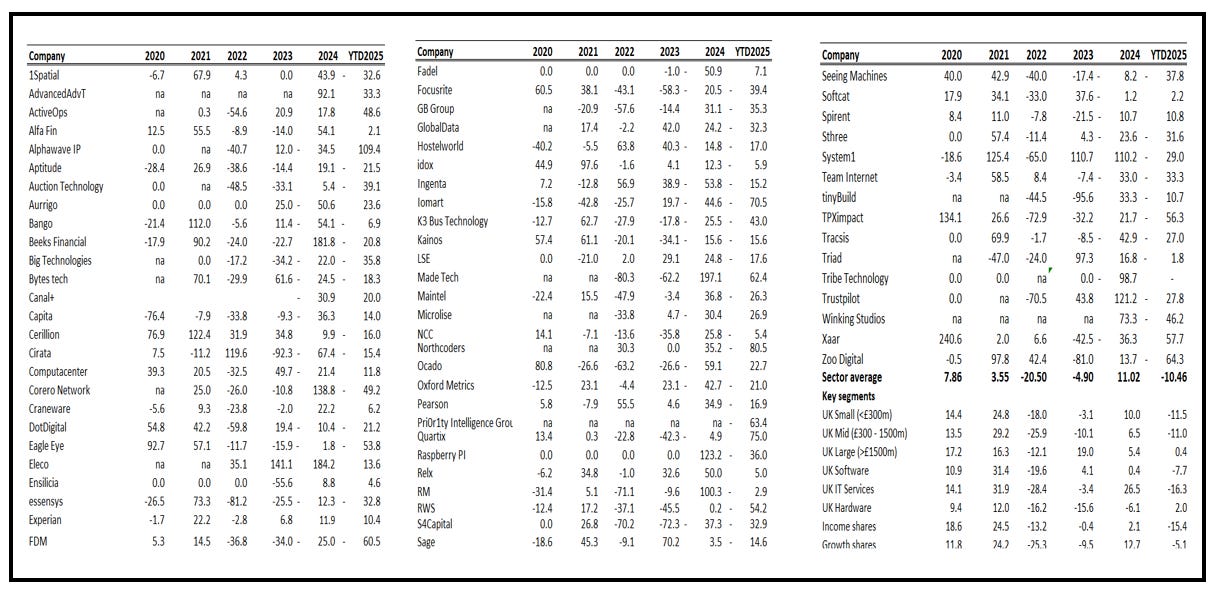

Tracking TSR across the UK listed company group

Note: Priced 15 August pre-market. Source: Company data, Yahoo Finance, Technology Investment Services

Index performance, small falling behind

Note: Priced 15 August pre-market. Source: Company data, Yahoo Finance, Technology Investment Services

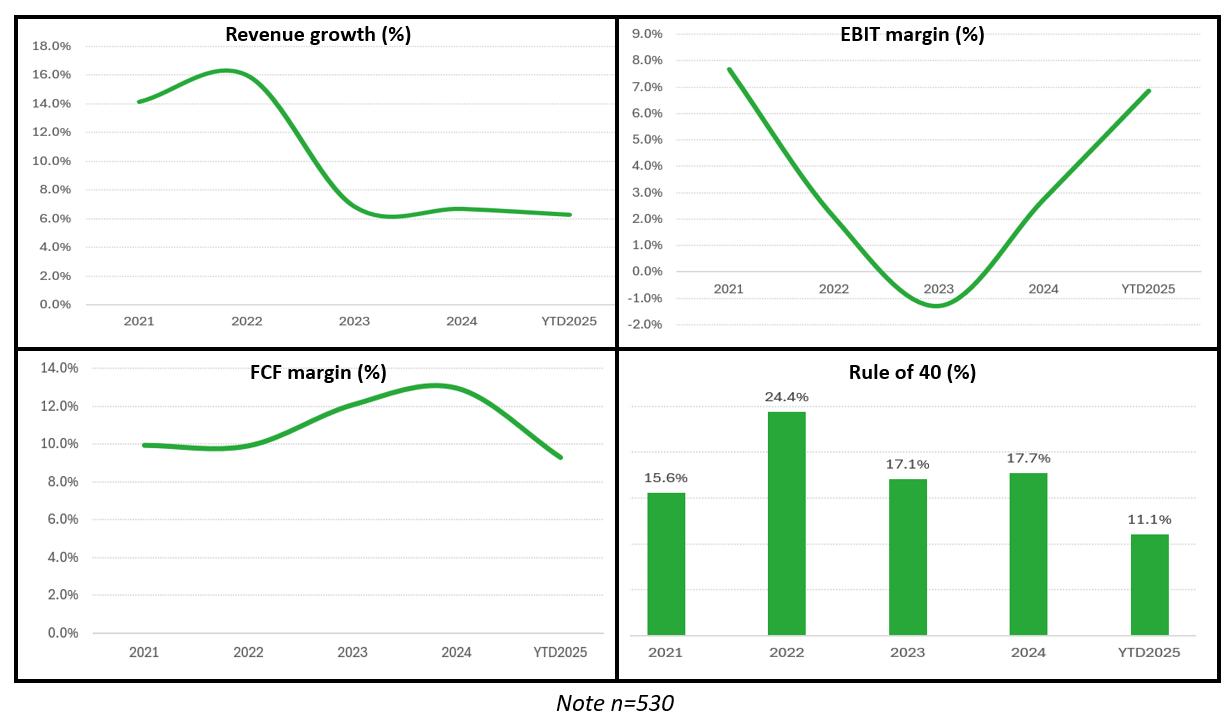

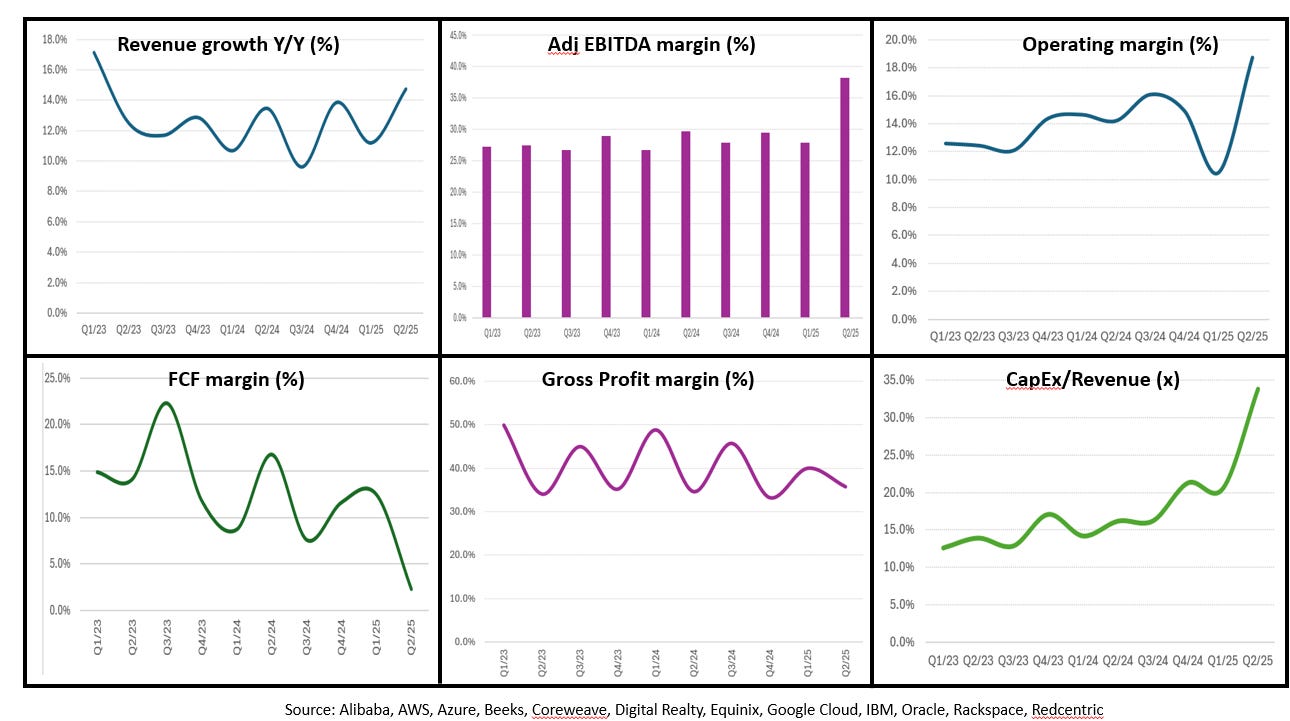

2. Tech sector overall KPIs in the midst of Q2 reporting

Note n=530. Source: Company data, Technology Investment Services

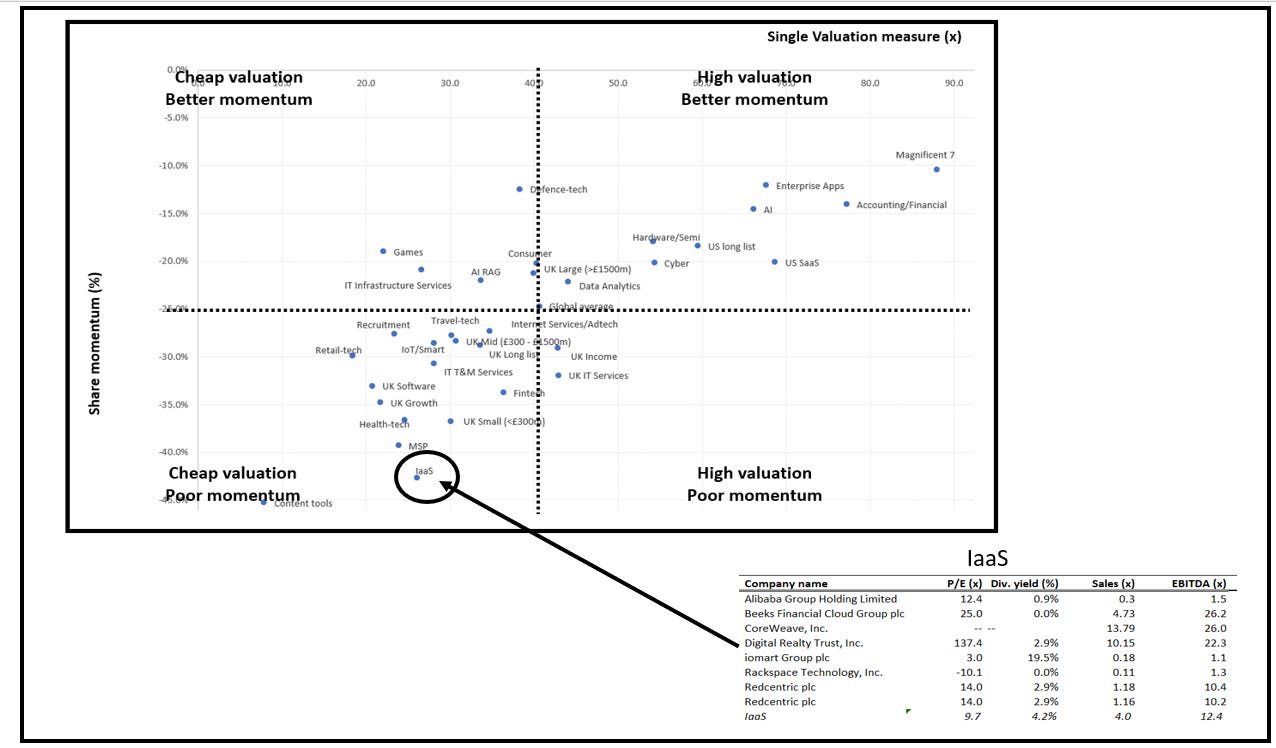

3. Valuation and share momentum for this months in focus cohort: IaaS is cheap and lacking momentum - Why?

Note: Priced 15 August pre-market. Source: Company data, Yahoo Finance, Technology Investment Services

Company news & Updates

IoT/Smart

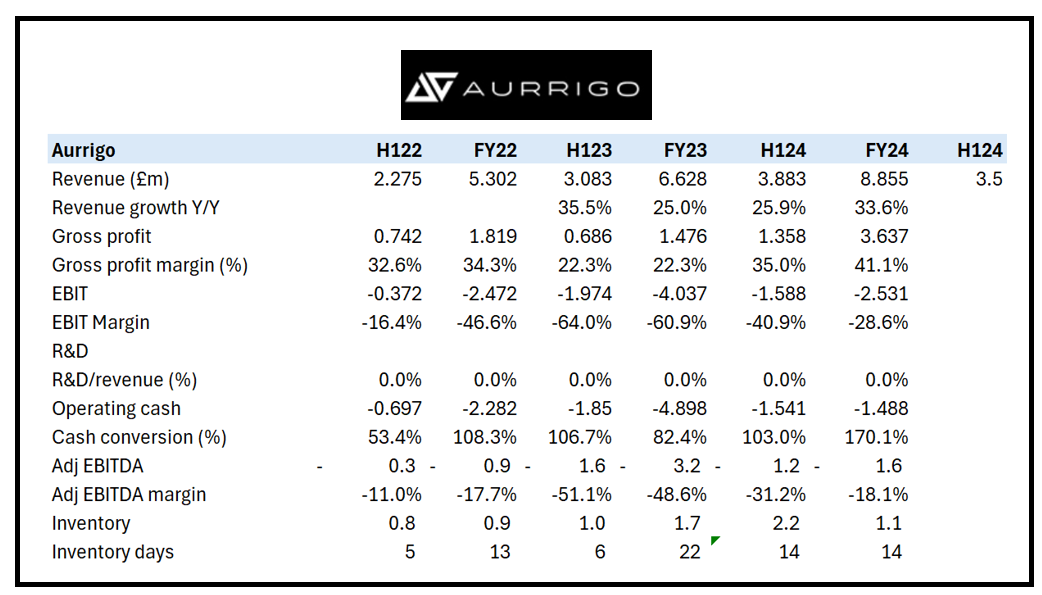

Aurrigo. Profit warning. H1 is “broadly in line” with £3.5m revenue, down from £3.9m last year. Autonomous division revenue £1.14m +41% Y/Y, Automotive division revenues of £2.36m from £3.1m Y/Y as US tariff on UK car OEM production volumes. Looking to H2 the company guides that the US tariffs will continue to weigh on the Automotive division. Consequently H2 revenue is guided to be flat sequentially (i.e. £3.5m) compared with consensus £12m, with EBITDA “materially impacted” vs consensus -£1.6m. Cash (30 June) £1.8m. Post period end the Group was awarded new grant funding (£1m) to advance new autonomous transport innovations. The funding is being provided by The Connected and Automated Mobility (CAM) Pathfinder - Enhancements programme.

The numbers we track: Aurrigo

Source: Company data, Technology Investment Services

UK Hardware

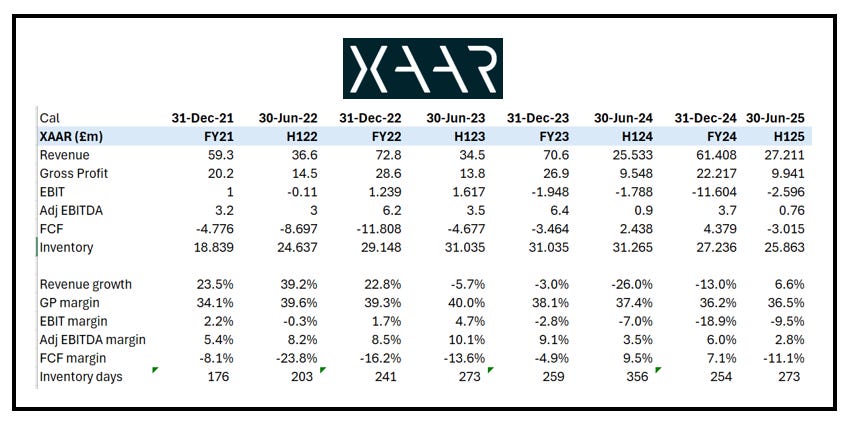

Xaar. ‘Growth cures all ills’. Interim results headline with a return to revenue growth, +7% Y/Y, with Printhead revenue +20% Y/Y. Growth was achieved against a backdrop of uncertainty, tariffs and challenging trading conditions, so while the print is positive, caution remains. Revenue in the first of Xaar’s four target focus markets, jewellery wax, soared from £0.6m last year to £3.3m. This is a telltale about Xaar’s ‘secret sauce’: its unique product portfolio coupled with an improved ability to execute. Xaar is currently celebrating its 35-year anniversary, a party extended to Capital Markets where the shares are 72.5% YTD. While some of the trading KPIs continue to urge caution for the immediate term, there are positive signs, although much depends on the exact timing of OEM product launches. Investors have not missed this rising star: shares trade on a pedestrian 1.3x EV/Sales vs. sector 3.1x – the re-rating is long overdue, in our view.

See our coverage on Progressive Equity Research

The numbers we track: Xaar

Source: Company data, Technology Investment Services

IaaS

IaaS cohort: KPI dashboard - a curate’s egg of good and bad and so uncertainty weighs on valuation and momentum

Source: Company data, Technology Investment Services

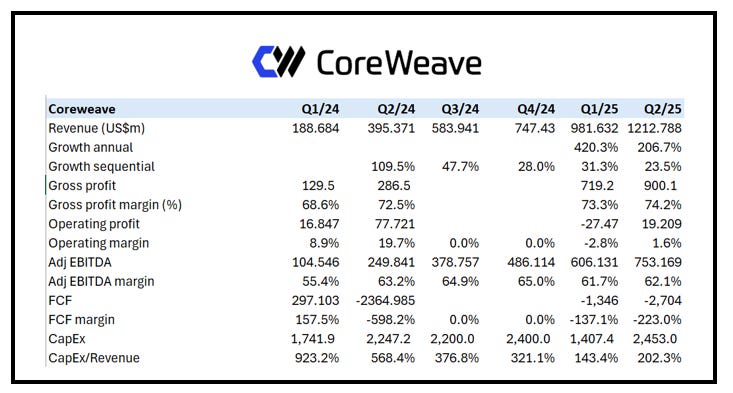

CoreWeave. Shares continue to fall in the wake of Q2 results and have lost about half its peak market cap due to:

servicing debt costs resulting in a higher-than-anticipated loss,

understandable profit taking on the print with shares after a 148% gain YTD coupled with the end of lock up period for insiders, and

guidance of US$20–$23bn in capex for 2025, with a “significant portion” coming in Q4, so concerns about an expensive share.

Q2 revenue +207% Y/Y, EBIT margin 1.6% with Adj EBITDA margin 62%. There is also a revenue backlog (defined as RPO and other amounts under committed customer contracts) of US$30.1bn at 30 June, which was up from US$16.2bn 12 months ago. Key customer wins in the period included a US$4bn expansion deal with OpenAI which was in addition to previously announced US$11.9bn deal a new unnamed new hyperscaler customer and AI labs and enterprise customers including: BT Group, Cohere, Hippocratic AI, Hologen, LG CNS and Mistral. There is the continuous scaling of the purpose-built AI Infrastructure and CoreWeave ended the quarter with c.470 MW of active power and increased total contracted power c. 600 MW to 2.2 GW across 33 data centres. Raised US$2bn in 9.25% Senior Unsecured Notes (due 2030) which was upsized by US$500m due to strong demand. Michael Intrator, Co-Founder, Chair and CEO commented that Coreweave is the first company to “offer the complete Blackwell GPU portfolio at scale, making CoreWeave the platform of choice for the world’s most advanced AI workloads and AI pioneers”.

The numbers we track: CoreWeave

Source: Company data, Technology Investment Services

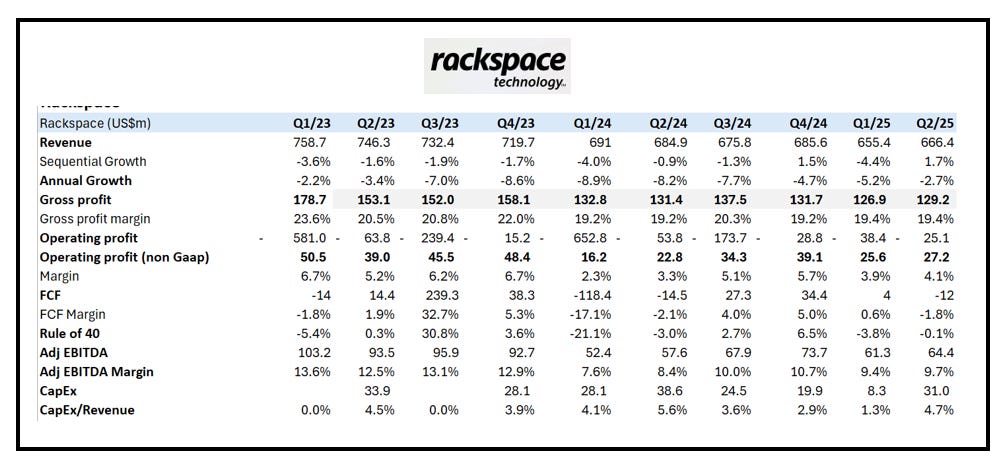

Rackspace. The operational turnaround continues apace - leaving investors to ponder when to buy a turnaround for the expected double whammy of improved earnings and re-rating. Q2 revenue, -3% Y/Y to US$666m, with Private Cloud revenue (US$250m) -4% Y/Y and Public Cloud (US$417m) -2% Y/Y. CEO Amar Maletira reminded that “revenue and operating profit exceeded the midpoint of guidance and EPS was within our guided range” (note: expectations for the 12th consecutive quarter) and that Bookings grew 16% while operating profit +34% Y/Y. Shares were positive in the aftermarket, recovering some of the losses of the year – shares are -45% YTD - but sentiment still seems weak.

The numbers we track: Rackspace

Source: Company data, Technology Investment Services

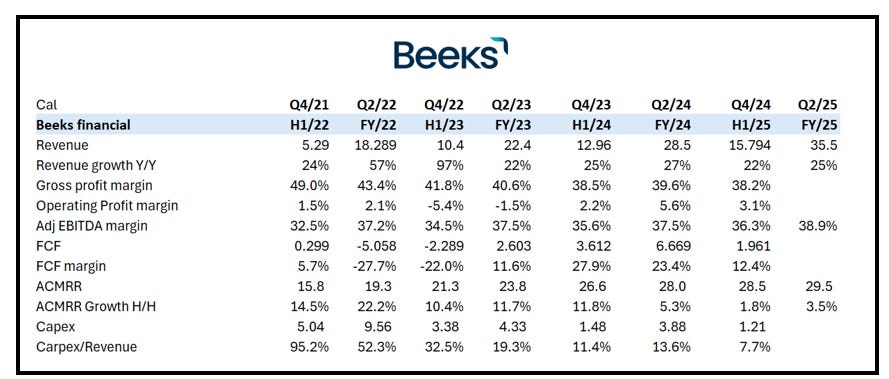

Beeks Financial. Yesterday’s (13 August) release of Market Edge Intelligence marks the debut of the ‘world's first AI/Machine Learning solution for passive monitoring of capital markets data directly at the network edge’, according to Beeks. While other monitoring tools (Corvil) are available, this is the first specifically developed for this market and use case. This product creates expansion opportunities, widens TAM, and is a great price lever adding to the already substantial recurring revenue pool at Beeks

Read our full coverage at Progressive Equity Research

The numbers we track: Beeks

Source: Company data, Technology Investment Services

Recruitment

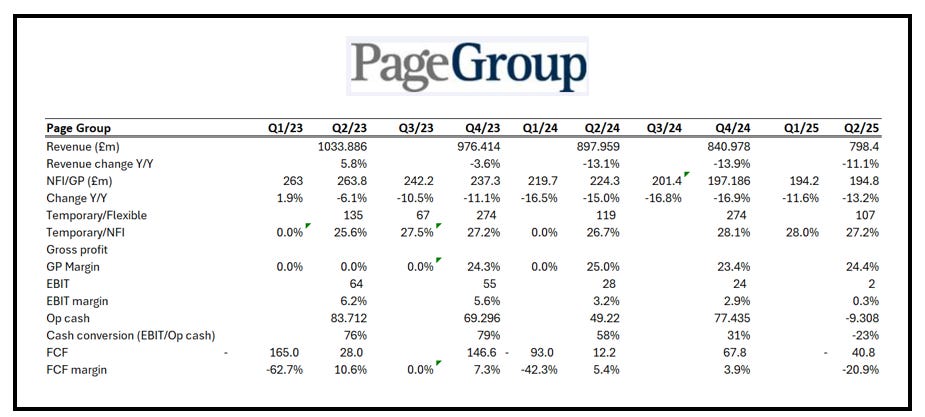

PageGroup. H1 results featured gross profit down 9.7% to £389.7m but EBIT, £2.1m, collapsed from £28.4m last year. This follow the £13m one-off restructuring (207 roles cut in H1) and transformation costs – there is a further £2m expected in H2 leading to annualized £15m cost savings. Net cash £10.8m, down from £57.2m last year, with the DPS, 5.36p, unchanged. Note:

Gross Profit from the regions: EMEA (54% of Group) £208.9m -16.0% Y/Y, Americas (19% of Group) £74.9m -3.1% Y/Y, Asia Pacific (15% of Group) £59.3m, -7.7% Y/Y, UK (12% of Group) £46.6m, -13.4% Y/Y.

For the six month period Gross profit from Permanent £282,278 from £325,520 last year while Temporary £107,379 was down from £118,621 last year.

Also for the six months period Gross Profit by discipline was: Accounting and Financial Services was £134,439, down from £145,664 Y/Y; Technology £46,546, down from £58,602 Y/Y; Legal, HR, Secretarial and Other £59,232, down from £71,067 Y/Y; Engineering, Property & Construction, Procurement & Supply Chain £98,002, down from £110,712 Y/Y; Marketing, Sales and Retail £51,438, down from £58,096 last year.

There are “continued subdued levels of client and candidate confidence impacted decision making”. Guidance is that the 2025 EBIT to be “broadly” in line with consensus, i.e. c.£22m. CEO Nicholas Kirk commented that while activity levels “remained robust across most of our markets” the company saw a “slight deterioration in activity levels and trading in Continental Europe towards the end of the period, particularly in our two largest markets, France and Germany”. However there was “some improvement” in activity, trading and customer confidence in Asia and the US”. Permanent recruitment continued to be impacted more than temporary, as clients sought flexible options and permanent candidates remained reluctant to move jobs.

The numbers we track: PageGroup

Source: Company data, Technology Investment Services

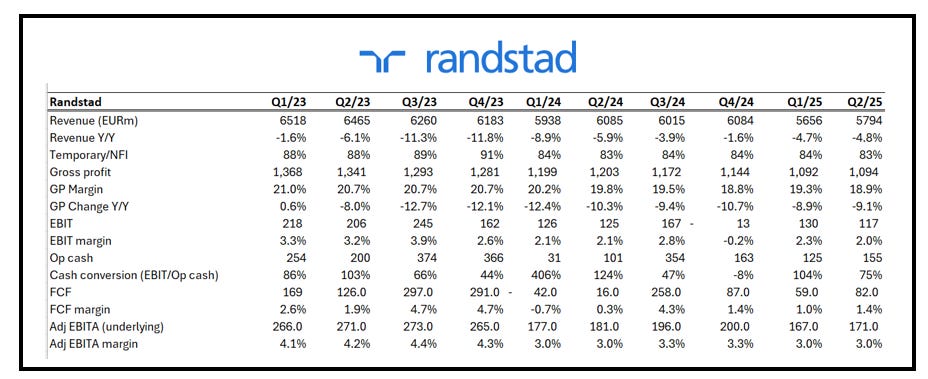

Randstad. Q2 results saw revenue -4.8% Y/Y to € 5,794m, with organic revenue/working day -2.3% Y/Y, however in Q1 this was -4.2%. By geography revenue/working day in North America (-1 %), Northern Europe (-4%), Southern Europe, UK and Latin America (-3%), but AsiaPac + 2% a reversal from the 1% fall in Q1. Perm fees were -13% Y/Y, an improvement from the -14% in Q1, RPO (Recruitment Process Outsourcing) fees + 8% YY, accelerating on Q1 rate at 5%). Operating profit was €117m from €125m last year.

Looking at the ‘shape’ of revenue by the operational disciplines (I’m looking for further evidence of the ‘staffline approach’ – i.e. surf the shift in employment from white to blue collar – possibly a GenAI employment effect?) Randstad Operational revenue was €3,848 -3% Y/Y, Randstad Professional €955 -9% Y/Y, Randstad Digital €655 -6% Y/Y, Randstad Enterprise €336 -5% Y/Y with online Monster being disposed of last year. (Note: Mea culpa the print was 23 July but was in the wrong part of my diary #analystfail).

The numbers we track: Randstad

Source: Company data, Technology Investment Services

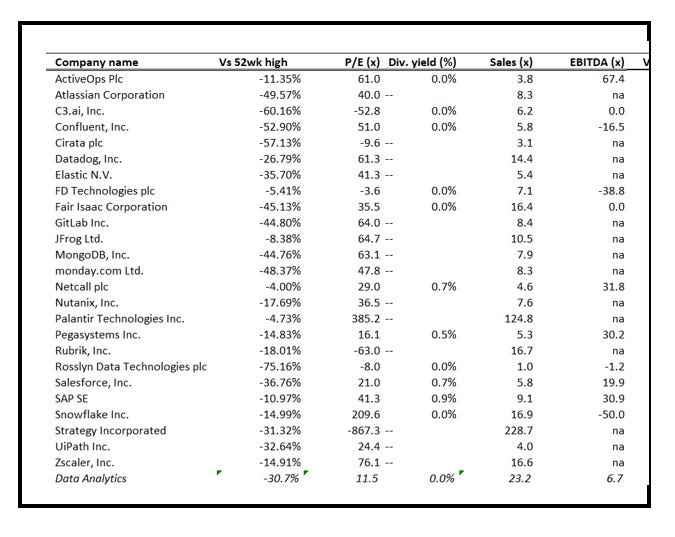

Data & Analytics

Monday.com. (“Traditional work software is broken” with 245k customers across 200+ markets as it strives to become “the go-to work platform for business”) revenue, US$299.0m, +27% Y/Y, EBIT loss -US$11.6m vs a US$1.8m last year. Operating cash US$66.8m, with US$64.1m Adj FCF compared to US$50.8m Adj FCF last year. Monday.com Co-founders and co-CEOs Roy Mann and Eran Zinman commented that the new AI capabilities “address core challenges across all our product areas and allow users to focus on their most critical strategic priorities”. CFO Eliran Glazer added that the company is focused “on the factors we can control”. NRR dipped to 111%, but has a range from 110%. I remain a fanboy, but I appreciate that the cohort is under pressure from the perceived impact of AI natives, despite weaving in AI across the product set. These companies were all disrupters and now for some the tables are turning.

Data & Analytics cohort: Valuation snapshot (x)

Note: Priced 15 August. Source: Company data, Yahoo Finance, Technology Investment Services

IT Infrastructure Services

Cancom. Following the prior warning, Cancom posted H1 results. The headlines were in line with revised guidance, and featured a 3.8% Y/Y fall in revenue, EBITDA down 33.9% Y/Y (margin 4.6%, 6.6% last year. The company says that despite the challenges which led to the recent warning the market has started to stabilize and “signs of recovery are visible”. There was a further ‘leg down’ for the share price on the open following the news. While we have heard elsewhere of some burgeoning recovery in Germany, it seems premature to get too excited - corporate buyers will frequently use weak market conditions to trade up their supplier pool.

IT Professional Services

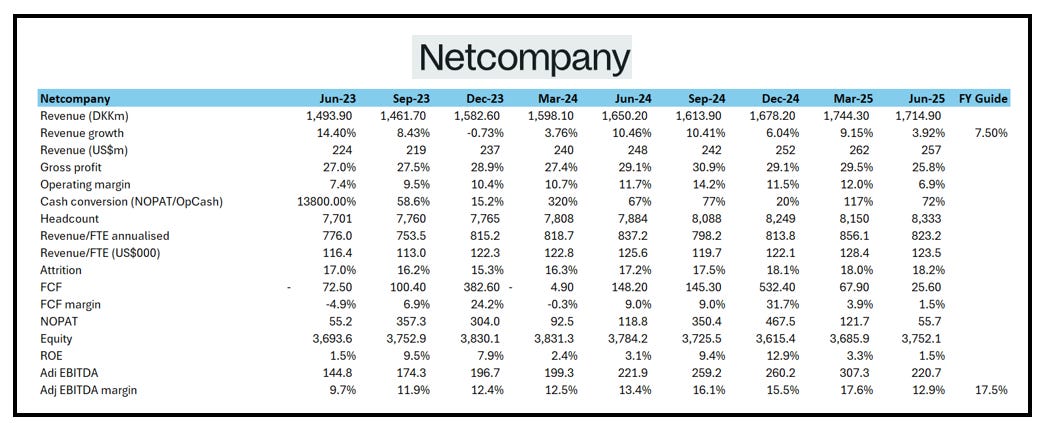

Netcompany. Reported revenue grew 3.9% Y/Y, -1.7% sequentially. There was 4.4% Y/Y growth in the public sector, with the private sector lower at +2.8% Y/Y. Revenue growth was negatively impacted by the Danish business segment (Denmark revenue -3.9% Y/Y) as it allocated product and business development and prepared for the integration of SDC into Netcompany Banking services (transaction closed 1 July). Issues on resourcing, and fewer days saw the profit KPIs fall with Gross Profit, EBIT and Adj EBITDA margins all down sharply Y/Y (see data below). This was despite Freelancer FTEs -7.9% Y/Y to 847 following a decrease in freelancers in Netcompany SEE & EUI. To compound the negatives the decrease in EBIT coupled with negative working capital resulted in FCF falling to DKK25.6m, from DKK148.2m last year. UK revenue was up to DKK160.1m, from DKK145.1m last year, however the UK pattern mirrored Group with Gross profit margin down from 15.6% to 14.0%, and EBIT loss, -DKK8.4m, reversing the DKK0.4m profit last year. The company reiterated FY guidance: revenue midpoint 7.5% (7.4% last year), Adj EBITDA mid-point 17.5% (16.9% last year). As this is ahead of the cohort wide guidance (FY25 guidance revenue growth 3.65% reported) and so is more than likely to be dismissed by the investment community, for now. Yet Europe’s re-arming continues, there is greater political stability making easier Public Sector ‘comps’ so the ‘stretch’ is not as extreme as the numbers suggest. Shares are +0.5% (-30% YTD) as I write (14 August) - keep an eye for any late in the year share price bounce.

The numbers we track: Netcompany

Source: Company data, Technology Investment Services

Gaming

Trufin. Raising FY expectations – providing further evidence of a return to form in the gaming sector - fingers crossed. H1 trading (6 months to 30 June) headlines with revenue c.£35.5m, +40% Y/Y with the performance due to momentum within the Playstack division (Publisher and in house). Adj EBITDA expected to be “more than £6.7m”,i.e. >125% Y/Y with Group PBT “more than £4.7m”, i.e. >670% Y/Y. As a consequence performance is set to “materially exceed market expectations for the full year”. In addition H2 started strongly, helped in particular by the full launch of Abiotic Factor at Playstack in July 2025. With a growing back catalogue, strong return on invested capital track record, and impressive pre-launch data from its secured games pipeline, CEO James argues that Playstack is well-positioned for 2025 and beyond.

Travel-Tech

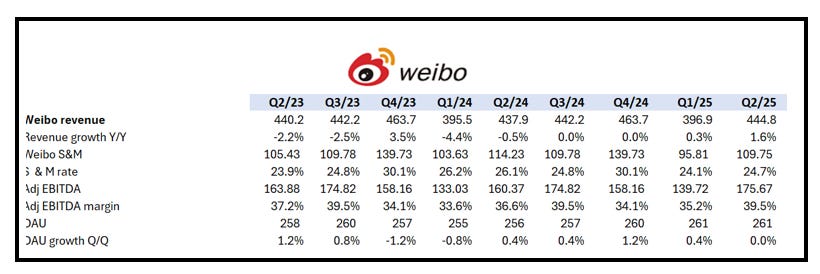

Weibo. Q2 revenue US$444.8m +2% Y/Y, EBIT US$145.6m, +8% Y/Y as Average daily active users ("DAUs") were flat sequentially at 261m. Revenue and profit were ahead of expectations. Gaofei Wang, CEO commented that quarter was focused on the “integration of social products and upgrade of recommendation system, which are aimed at improving user engagement and content consumption on the platform” as the user community AI-powered intelligent search “grew robustly”. The mention of AI driven growth seems to be the reason for the strong share rally in the wake of the print.

The numbers we track: Weibo

Source: Company data, Technology Investment Services

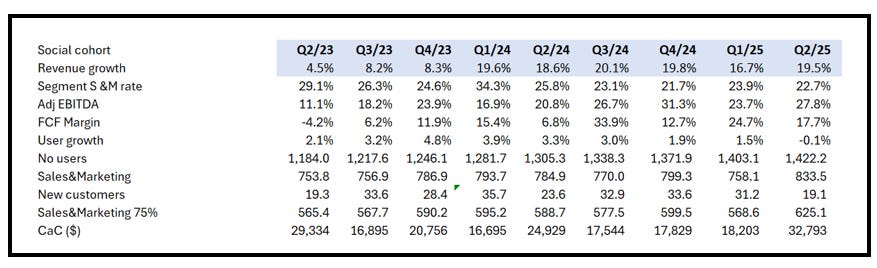

End note: To remind. We track Weibo, and the social cohort, because OTA companies are increasingly using‘social’ products, GTM and ‘social’ overall ‘look and feel’. As a consequence their financial KPIs will follow. (We appreciate that this is not a rabbit hole (err Reddit hole!) that the mainstay of the investor community look at.) My concern about the lessons from the social cohort from Q2 is that CaC is getting somewhat out of control - see below. It is too early to draw too many conclusions, and admittedly this is somewhat stock specific (i.e. an outsized influence by Pinterest) but the attraction of the social financial model deteriorated in Q2.

Social cohort: KPI data

Source: Company data, Technology Investment Services

Dear investor,

Thank you for reading to the end. Don’t forget to subscribe if you haven’t already!

Join me again soon.

Best wishes

George

End notes & Disclaimer: Please read

All information used in the publication of this report has been compiled from publicly available sources that are believed to be reliable, however we do not guarantee the accuracy or completeness of this report and have not sought for this information to be independently verified. This is not investment advice. Opinions contained in this report represent those of the author at the time of publication. Forward-looking information or statements in this report contain information that is based on assumptions, forecasts of future results, estimates of amounts not yet determinable, and therefore involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of their subject matter to be materially different from current expectations. The author is not liable for any direct, indirect or consequential losses, loss of profits, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained herein. The information should not be construed in any manner whatsoever as, personalized advice nor construed by any subscriber or prospective subscriber as a solicitation to effect, or attempt to effect, any transaction in a security. Any logo used in this report is the property of the company to which it relates, is used here strictly for informational and identification purposes only and is not used to imply any ownership or license rights between any such company and Technology Investment Services Ltd. Email addresses and any other personally identifiable information collected in the provision of the newsletter are only used to provide and improve the newsletter.

Need more

Let’s chat at Progressive Equity Research where I am delighted to be a contributing analyst and my website.

The ask

My name is George O’Connor. I am a tech investment and IT industry analyst. I explore shareholder value, its drivers, the best exponents, the duffers. The target readers are investors, companies, advisors, stakeholders and YOU. If you like this please subscribe and pass it on to colleagues and friends. That said, if you hate it - do the same. Thanks for dropping by dear investor.