The long and the short of IT

The long and the short of IT

Computacenter IT Services: “Half-full/half-empty? I ordered a cheese burger”

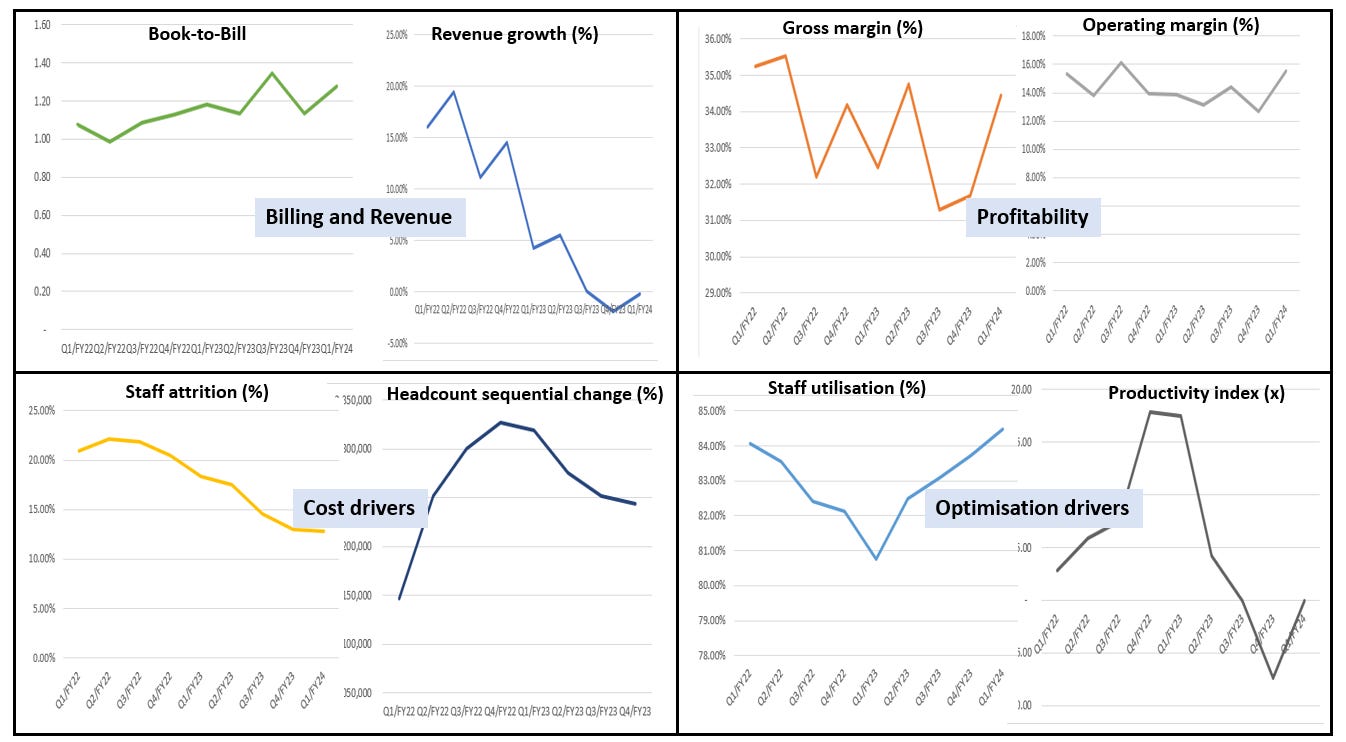

Computacenter Q1 Update (1 May) saw trading “in line”. Technology Sourcing returned to normal (natch: check the industry shipment - below), IT Profession Services has a growing pipeline but there was a run-off in Managed Services contracts. Computacenter did not comment on cash (or capital allocation – darn, monster cash pile). As we scan global Professional Services peers, we note that concerns about broad-based weakness are abating, the majority see Q1/Q2 2024 as the trough and their thinking is supported by a strengthening book-to-bill, improving utilisation, productivity, revenue/head, COGS and declining input inflation. All experienced GenAI as a growth accelerator. Capgemini had a record Q1, at CGI the UK (and Australia, bonzer) were the standout performers. There were positive/not deteriorating comments from Sopra and Tieto with similar messages repeated by HCLTech, LTIMindree and Tech Mahindra. We too are cautious about Financial Services and Manufacturing sectors, and AWS (Q1, 30 April) spoiled the mood with its “we continue to keep an eye on consumer spending and macro level trends, specifically in Europe, where it appears to be a bit weaker relative to the US”. The business environment favours operational agility & cost-efficiency but this should nudge to more strategic, discretionary and growth-focused as 2024 progresses – macro permitting. Here, we tease out the KPIs from the latest reporting group as we update our IT Professional Services dashboard. Spoiler Alert: Revenue growth is still drifting lower (that’s about vanity) as are headcount and attrition, but the majority of (sanity-based) KPIs are trending better. Good news: Valuation remains a tailwind.

Computacenter Q1 Trading (1 May): Reiterates FY Guidance

Computacenter reiterated FY guidance following a “broadly in line” Q1 (ended 31 March). From the regions: Germany and North America delivered solid underlying performances - Germany is 29% and North America is 40% of Group revenue, 56% and 22% of EBITA respectively. However, “the UK remained challenging”. From the portfolio:

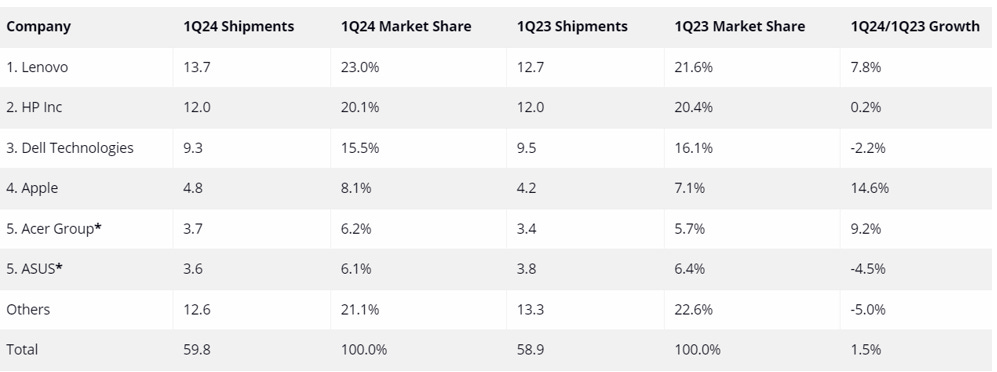

Technology Sourcing (76% of group revenue) “returned to more normal levels” with higher-volume, lower-margin contracts in North America and the excellent growth achieved in Germany in the prior year. Towards the end of Q1 it won a “significant new Technology Sourcing contract” with a large US customer which starts to the end of Q2. Computacenter has a strong and growing pipeline in North America for the rest of the year. Industry data (below) shows Q1 PC shipments +1.5% Y/Y, a small number but a massive turnaround - this time last year PC shipments were -29% Y/Y.

Services (24%) revenue was below Y/Y with “continued growth in Professional Services” (10% of Group revenue) outweighed by the expiry of certain Managed Services contracts (14%). At the beginning of Q2, Computacenter started a large four-year public sector contract in the UK. The pipeline of Professional Services opportunities across the Group is “encouraging” - the peer evidence suggests that it should be.

For the outlook commentary, H1 Adj PBT is guided as down Y/Y, but the strength of the integrated Technology Sourcing and Services model, order backlog and pipeline, saw Computacenter re-iterate FY guidance. Remember, Computacenter group margins suffered from Professional Services, but this is being addressed on an industry-wide basis – our mean revision thinking suggests this is where there is margin upside.

Dates for your diary. Capital Markets Day: Afternoon 5 June and H1 results 9 September.

CGI Q2 (1 May): UK as the global standout performer

Q1 UK and Australia revenue CAN$402.2m up from CAN$368.3m, implying 5.1% cc growth. EBIT CAN$64.5m, from CAN$55.3m Y/Y reflects a 16.0% margin (15% Y/Y). This was in line with the general upward trend that we see across the IT Professional Services spectrum. The UK 5.1% CC revenue growth was the standout across the group. Remember the former brands Logica, CMG, Admiral are hiding out in CGI so there is a long-established UK customer franchise here. From a vertical market perspective Banking was weak (a message repeated widely), with public sector stronger – a note that this bodes well for Kainos (reported), Made Tech and TPXimpact, but we expect cautions in their outlook statements given the UK election cycle.

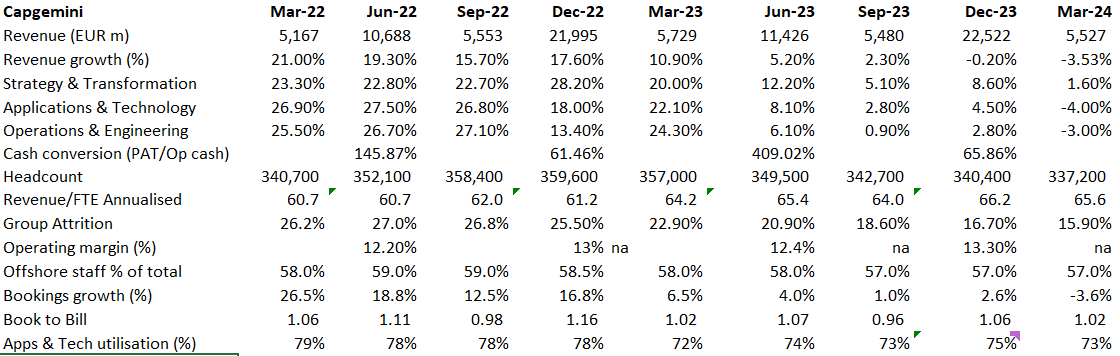

Capgemini: Q1 (30 April): A record quarter

Q1 revenue €5,527m, -3.3% Y/Y cc. Of the geographies North America (28% of Group revenue) was -7.1% Y/Y with Financial Services and TMT sectors contributing most to this decline. The UK/Ireland (12% Group) revenue was -3.2% Y/Y, and again mostly due weakness in Financial Services and TMT sectors with Services and Energy & Utilities sectors sporting “solid momentum”. The commentary from CEO Aiman Ezzat: “As anticipated, the market continued to slow down in Q1, and we confirm the growth trough is now behind us. We expect the market to gradually pick up toward an attractive exit growth rate in Q4, setting up for a more tangible acceleration in 2025.”

Sopra Steria: Q1 2024 (26 April) In line

Q1 revenue €1,587.4m +13.8% Y/Y of which organic growth was 0.3%. The company re-confirmed FY organic growth, operating margin rate and free cash flow guidance. CEO Cyril Malargé commented that the environment was marked by a slowdown in discretionary investments and the most resilient sectors were the public sector, financial services and defence. The UK (15% of Group) recorded €240.0m revenue, with 7.4% organic growth and growth was driven by a “very robust public sector and a private sector that started to feel the positive effects of new contracts signed in the H2/2023, which will gradually ramp up over the course of 2024”.

Tietoevry: Q1 (25 April): In line

Q1 revenue growth -2% Y/Y was impacted by a “soft macroeconomic environment, high comparison figures and fewer working days”. Tieto reiterated FY guidance (the headlines are organic growth 0–3% and Adj EBIT margin 12.0 – 13.0% ,12.6% Y/Y). Tieto is a Scandinavian and Eastern European SI and software company where it views the addressable market growing by a tepid 0–2% this year. Note: (i) There is little UK presence, the beating heart is Sweden (3,804 FTEs), Norway (3,817) and Finland (3,004), (ii) The company is selling its Tietoevry Tech Services division (Q1 revenue €263.3m, -9% Y/Y) which is “progressing as planned”.

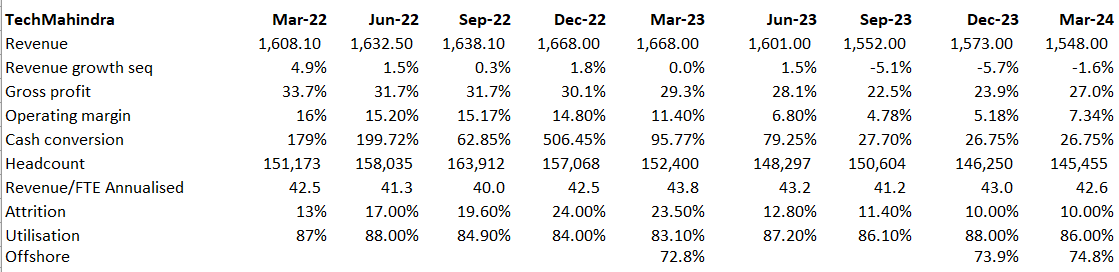

Tech Mahindra Q4 (25 April): In line

Q4 and FY results (ended 31 March) were in line but guidance was muted. The company reported Q4 revenue US$1,548m being -1.6% Q/Q (Europe was the outlier being +0.1% Q/Q). EBITDA, US$169m being + 22.9% Q/Q, -31.1% Y/Y with the margin, 10.9%, +220 bps Q/Q. CEO and MD Mohit Joshi: “As we step into FY'25, we look forward to improvement in clients spending, which fuels our optimism for a better revenue performance ahead. . . FY'24 posed its fair share of challenges for the IT services sector; yet, amidst the global economic uncertainties, we continue to observe a notable push towards digital adoption.”

HCLTech Q4 (26 April): In line

Q4 revenue US$3,430m +0.4% Q/Q and +6.0% Y/Y, Services revenue +3.0% Q/Q, +6.7% Y/Y “led by growth in Telecommunications, Media, Publishing & Entertainment (+ 21.6% Q/Q) with Digital revenue +6.3% Y/Y. From the CEO and MD C Vijayakumar; “As we look ahead, global enterprise technology spend will only grow with adoption of AI. We are well positioned to capitalize with our AI led propositions, Global delivery model and ideal mix of technology services and products.”

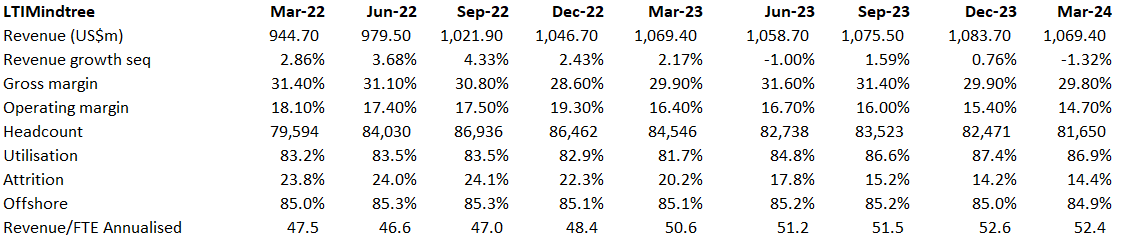

LTIMindtree Q4 (24 April): In line

Q4 revenue US$1,069.4m, which was -1.3% Q/Q and +1.1% Y/Y with Net Profit US$132.4m, -5.8% Q/Q and -2.4% Y/Y. CEO and MD Debashis Chatterjee: “We closed FY24 amidst a tough macro environment and delivered a resilient performance . . . As the market dynamics evolve, we are excited to be part of innovations, partnerships, and initiatives that our clients will embark on in FY 25.”

The data

PC shipments have recovered, at last

Source IDC, April 2024

Capgemini: The scorecard

Source: Company data

Tieto: The scorecard

Source: Company data

SopraSteria: The scorecard

Source: Company data

CGI: The scorecard

Source: Company data

HCLTech: The scorecard

Source: Company data

LTIMindtree: The scorecard

Source: Company data

TechMahindra: The scorecard

Source: Company data

IT Professional Services dashboard

Source: Company data, Analyst

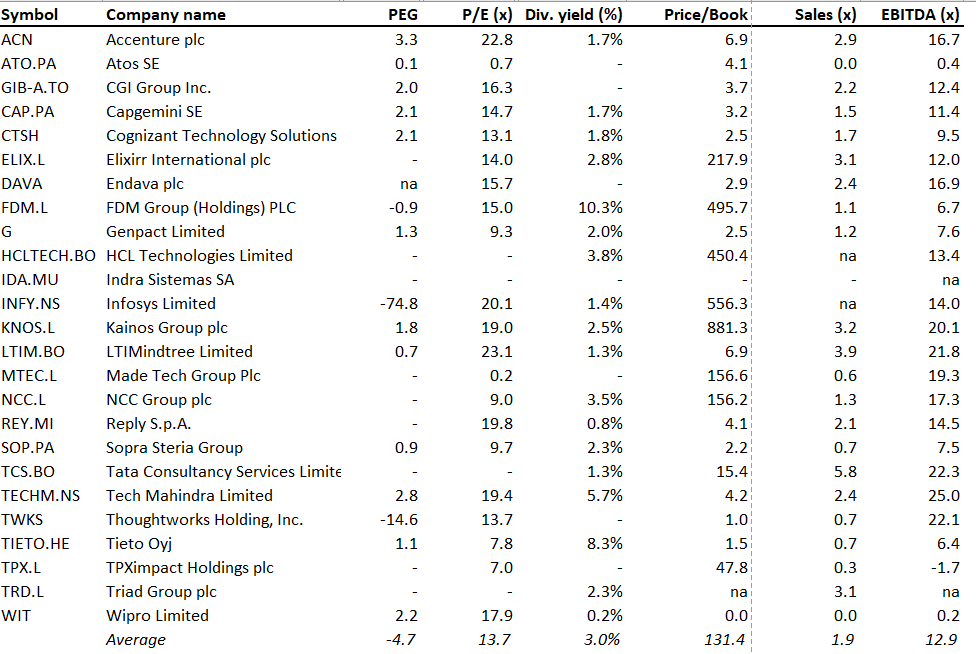

IT Professional Services cohort: Valuation overview

Source: Company data, Yahoo Finance, London South East, Analyst

End notes & Disclaimer: Please read

All information used in the publication of this report has been compiled from publicly available sources that are believed to be reliable, however we do not guarantee the accuracy or completeness of this report and have not sought for this information to be independently verified. This is not investment advice. Opinions contained in this report represent those of the author at the time of publication. Forward-looking information or statements in this report contain information that is based on assumptions, forecasts of future results, estimates of amounts not yet determinable, and therefore involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of their subject matter to be materially different from current expectations. The author is not liable for any direct, indirect or consequential losses, loss of profits, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained herein. The information should not be construed in any manner whatsoever as, personalized advice nor construed by any subscriber or prospective subscriber as a solicitation to effect, or attempt to effect, any transaction in a security. Any logo used in this report is the property of the company to which it relates, is used here strictly for informational and identification purposes only and is not used to imply any ownership or license rights between any such company and Technology Investment Services Ltd. Email addresses and any other personally identifiable information collected in the provision of the newsletter are only used to provide and improve the newsletter.

Need more

Let’s chat at Progressive Equity Research here where I am delighted to be a contributing analyst and my website here.

The ask

My name is George O’Connor. I am a tech investment and IT industry analyst. I explore shareholder value, its drivers, the best exponents, the duffers. The target readers are investors, companies, advisors, stakeholders and YOU. If you like this please subscribe and pass it on to colleagues and friends. That said, if you hate it - do the same. Thanks for dropping by dear investor.