The long and the short of IT

IT Professional Services: The fish in the tree

“If you judge a fish by its ability to climb a tree, it will live its whole life believing that it is stupid”. Software people can be ‘sniffy’ about IT Professional Services. Investors follow suit: currently rating services lower than their blousy IP counterparts (less than half EBITDA multiple – see below). While the IT services ‘Pull’ ratio has collapsed (see below & blame ‘cloud’) given the dominance of the few GenAI LLMs coupled with demand-side attributes that power balance may shift again. Ahead of that. The Services segment surpasses Comms to be world’s largest IT market this year. Over the past few days we enjoyed results from Professional Services firms: TCS (calQ1 opener from India), an FY trading update from Kainos, Q1 updates Robert Walters and PageGroup, interim results from Gattaca. All confirm the consensus: tech is soft. Look more closely you might discern a few positives: the ‘squigginess’ has not worsened, companies mutter “when demand recovers”, share price moves in a side-ways market betray little. Into that next phase, we pity the CIO who is navigating economic headwinds, trying to counter-balance a tight IT budget while attempting to ready the organisation for AI. Logically he/she must steal from other budgets to fund AI initiatives. The macro downer has depressed earnings and sentiment (higher for longer . . . blah blah) – they recover together, some in opposite directions. Ahead of that we review the latest.

Recruitment: Gattaca: “Starting to see growth in contract book”

Interim results (16 April) saw UK Net Fee Income (NFI – see it as gross profit, if you like) slide by 10% to £19.1m but the TMT segment grew by 10% . Admittedly the TMT comp helped, but the arrow moved in the right direction. In response to the conditions, Gattaca positioned deeper in Contract staff, now 76% of Group NFI, 68% this time last year, as Permanent NFI was down 36% Y/Y due to “challenging market conditions and against a strong comparative”. Positively:

PBT £0.8m was +100k Y/Y and,

net cash, £22.3m, up from £21.6m a year ago.

Gattaca commented that the macro-economic headwinds have impacted demand and candidate sentiment as it guided that permanent recruitment is likely to remain “subdued in the short term”. CEO Matthew Wragg added:

Investments in business development are starting to have a positive impact.

The company is seeing “high engagement, staff attrition below long-term targets and despite the market conditions, our productivity levels improving”.

While still cautioning that he has “yet to see signs of improvement” contract income has remained stable, and is starting to see “growth in our contract book”.

IT Implementation services: Kainos: “Core markets resilient”

In an FY Trading Update (15 April), Kainos guided that FY revenues (ended 31 March) are slightly below and adjusted PBT is in line with consensus forecasts. But the company has continued to be resilient in the economic climate, particularly in its Workday Products and Services segments. The statement suggested c5% revenue growth, from c24% Y/Y, with an Adj PBT margin up to c19%. That margin improvement combined with no DSO stretch (the industry is telling us that everyone is paying on time) suggests a positive impact on cash. That said our ‘wish’ would be a bigger-then-expected AI training spend - and thereby dovetail with the latest MCA findings that “AI, digital technology and cost reduction are the service lines expected to grow the most in 2024”.

Kainos commented the following in relation to its operational segments:

Digital Services - solid revenue performance and a strong sales performance and healthcare revenues continued to recover following the pandemic-related peak. Balancing this the commercial side was weak.

Workday Services - continues to generate good growth and,

Workday Products division recorded a “very strong” performance (note Workday next print is Q1 cMay23/24) both in the established products, Smart Test (for automated testing), Smart Audit (for compliance monitoring) and Smart Shield (for data masking), and in Employee Document Management. We see a product backlog at Kainos with a developing portfolio to sell into the Workday 10k customer base.

Kainos flagged that its core markets have proven to be resilient and offer substantial further growth opportunities, with its confidence is reinforced by “long-term customer relationships, and the caliber of our people”. In the near-term, it gains from an increased backlog, a “robust” pipeline and a strong balance sheet provide visibility of FY performance. Note: Into a Public Sector year end Kainos Public Sector (38% of revenue) will be splurging on budget flush (Public Sector budget 31 March) ahead of a slowdown around election (we are guessing November) lasting until the new regime gets comfortable - so anticipate some hand-wringing. Diary date: Finals 20 May 2024.

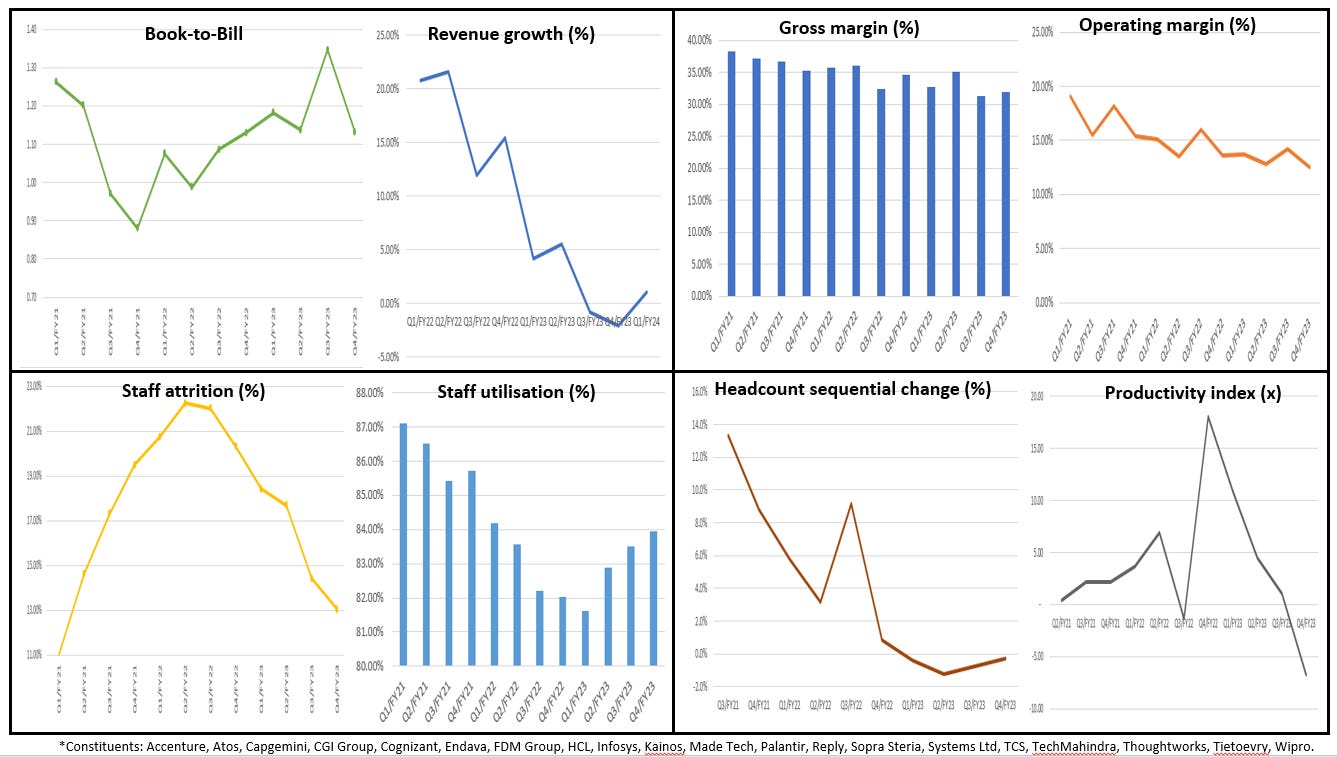

Note: We revised our IT Services dashboard (see below).

Recruitment: PageGroup: “UK NFI sequential improvement”

For its Q1 Trading update (15 April), Page stated that NFI was down 12.8% Y/Y. CEO Nicholas Kirk commented that “the slower end to Q4 2023 continued into Q1 2024, particularly within Continental Europe”. Overall activity levels remain strong despite the company experiencing “a slight deterioration in job flow towards the end of the quarter” with candidate and client sentiment being subdued “reflecting the general macro-economic uncertainty in most markets”. Like other recruiters the temporary division gained as clients sought more flexible options with temporary recruitment (-7%) permanent (-15%). The trading environment featured the slowdown from the end of Q4/2023 continued into Q1/2024 with some deterioration experienced, particularly within Continental Europe. Trading in Asia, the UK and the US saw “no improvement with low levels of client and candidate confidence” continuing to delay time to hire. Client' recruitment budgets tightened, and “offers made to candidates were not as elevated as they were in 2022 and early 2023”. UK Q1 NFI had a small sequential improvement being £27.1m -19.2% Y/Y in the wake of the 19.9% decline in Q4 2023. “We continued to see clients deferring hiring decisions and candidates cautious about accepting offers.” Note: Whether the disguised trend is a move back to the gig economy following the UK government flip-flop IR 35 implementation is unclear. At this juncture the lesson from history is that in a recession employers back-fill with temps rather than full time staff.

Recruitment: Robert Walters: “London NFI grows first time in 5 quarters.”

“Challenging market conditions” was the headline from the Q1 Trading update, 16 April. This surfaced in NFI which was down 21% to £81.3m with the UK (16% of Group NFI) £13.1m down 20% Y/Y. Here too we see the shift in emphasis to contractor as NFI from permanent was down 17% Y/Y with temporary down 10% Y/Y. The balance sheet is robust, net cash of £54m (31/3) but down from £79.9m (31/12/2023). As we dived into the segment data we noted that Asia-Pacific NFI was -16%, with Japan -4%, Australia -23%, New Zealand -28% but Mainland China +1%. Europe featured NFI -14% with France -15%, Netherlands -12% with the UK NFI down 20% Y/Y. However, Robert Walters commented that while trading conditions remain challenging fee income grew sequentially in London for the first time in five quarters. Toby Fowlston, CEO, commented: “although certain macro-economic indicators continue to moderate in some markets, the general environment remains one where client and candidate confidence is at low levels, which we expect to continue to be a headwind to fee income growth in the near-term".

IT Implementation services: TCS: “Growth led by the UK and Regional Markets”

TCS is the largest IT Services vendor in the UK and was the first to report calQ1 (ended 31 March), i.e. FYQ4 for TCS on 12 April. We note that the FY24 Order Book TCV is “at all time high” at US$42.7bn with a “record Q4 TCV”, US$13.2bn and growth was “led by the UK (+10.1%) and Regional Markets (+19.8%)”.

At group level Q4 revenue was US$7.36bn, +2.3% Y/Y, C/C 2.2%, with the 26% operatig margin being +150bps and operating cash flow was 100.4% of net income. Reviewing the capabilities we noted:

“Significant demand for Cloud, data platforms and Gen AI across industry segments” as clients “continued to scale their experimentation with Gen AI and went live with an increasing number of use cases”.

“Continued growth momentum” in Identity and Access Management (IAM), Governance Risk Compliance and Network Security and Platforms where TCS is “expanding footprint across all client segments, with clients seeking an integrated services approach to enterprise security”.

“Strong demand for Enterprise Application Services as clients make significant investments in their digital core through an ERP led Transformation approach”.

In IoT & Digital Engineering strong growth is led by multiple transformation programs and demand for next generation solutions across connected plants, connected services and intelligent product engineering. Key services leading the growth were Factory of the Future, Electric Vehicles and Software Defined vehicles, Digital thread, Digital Twins and Medical Devices Engineering.

We revised our IT Services dashboard (see below).

End note: Get exporting

Stop looking inwardly to the UK. The UK is great at Professional Services. The UK services sector accounts for 80% of GDP and employs 4 in 5 workers across the country. The UK is the world’s second largest exporter of services and the EU is the largest recipient – c40% of the UK’s total services exports.

The numbers guys at the Resolution Foundation conclude that the services sectors accounted for 56% cent of exports in Q3/2023, it was 30% in 1997. There is an issue (i) London dominates with a 46%: 2021 (38%: 2016) no leveling-up effect and (ii) recognising UK Professional qualifications following Brexit.

The data

The companies in this edition

Source: Company data, London South East, Factset, Analyst George O’Connor

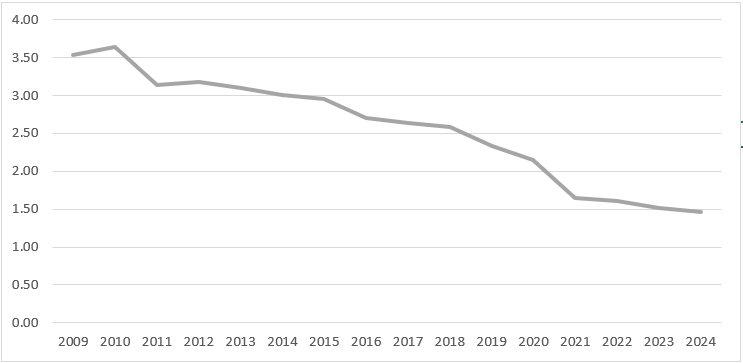

The IT Services Pull Ratio*

*Unit of Services sold for each software unit. Source: Analyst George O’Connor

The software valuation premium

Source: Company data, Factset, Yahoo Finance, Analyst George O’Connor

Significant issues for the consulting industry in the next 12 - 24 months

Source: MCA

IT Services Dashboard

Source: Company data, Analyst George O’Connor

Callout: TCS and the IT Services Dashboard

Source: Company data, Analyst George O’Connor

Kainos: KPIs since 2017

Source: Company data, Analyst George O’Connor

The IT Professional Services market taxonomy

Source: Company data, Analyst George O’Connor

The UK Export: Services beats product

Source: UK gov

End notes & Disclaimer: Please read

All information used in the publication of this report has been compiled from publicly available sources that are believed to be reliable, however we do not guarantee the accuracy or completeness of this report and have not sought for this information to be independently verified. This is not investment advice. Opinions contained in this report represent those of the author at the time of publication. Forward-looking information or statements in this report contain information that is based on assumptions, forecasts of future results, estimates of amounts not yet determinable, and therefore involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of their subject matter to be materially different from current expectations. The author is not liable for any direct, indirect or consequential losses, loss of profits, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained herein. The information should not be construed in any manner whatsoever as, personalized advice nor construed by any subscriber or prospective subscriber as a solicitation to effect, or attempt to effect, any transaction in a security. Any logo used in this report is the property of the company to which it relates, is used here strictly for informational and identification purposes only and is not used to imply any ownership or license rights between any such company and Technology Investment Services Ltd. Email addresses and any other personally identifiable information collected in the provision of the newsletter are only used to provide and improve the newsletter.

Need more

Let’s chat at Progressive Equity Research here where I am delighted to be a contributing analyst and my website here.

The ask

My name is George O’Connor. I am a tech investment and IT industry analyst. I explore shareholder value, its drivers, the best exponents, the duffers. The target readers are investors, companies, advisors, stakeholders and YOU. If you like this please subscribe and pass it on to colleagues and friends. That said, if you hate it - do the same. Thanks for dropping by dear investor.